An insurance adjuster in 2019 took 30 days on average to close a claim. In 2026, AI-powered insurers are doing it in 7.5 days. That is not an incremental improvement. That is a structural change.

Here is the number that frames everything else: the AI in insurance industry is projected to grow from $26.3 billion in 2026 to $114.52 billion by 2031; that makes it one of the fastest-growing technology deployments in financial services. And 91% of insurers globally have now integrated some form of artificial intelligence into their operations.

This is not a future story. It is a 2026 operational reality, and the gap between insurers who have embedded AI into their core workflows and those still running on legacy processes is measurable in revenue, loss ratios, and customer retention.

But here is what most AI in insurance industry gets wrong: it treats AI as a technology category, not a business decision. Whether you are a startup building an insurtech product or a CEO evaluating your digital transformation roadmap, the right question is not “what can AI do?” It is “which AI applications will move our specific numbers, and how do we build or buy them?”

This guide answers that question. It covers the real use cases of AI in the insurance industry with measurable outcomes and the 2026 trends that will separate the winners from the companies that treated AI as an experiment and never moved past the pilot stage.

What Is Artificial Intelligence in Insurance?

Artificial intelligence in insurance refers to the application of machine learning, natural language processing, computer vision, predictive analytics, and generative AI across the insurance value chain from underwriting and claims to customer service, fraud detection, and product design.

This is broader than automation. Traditional automation follows rules: “if claim type X, then action Y.” AI learns from data, identifies patterns, makes probabilistic decisions, and improves over time. That distinction matters enormously in insurance, where risk is inherently uncertain, and the data is rich but messy, structured and unstructured, historical and real-time, financial and behavioral.

The insurance industry is, in many ways, the ideal domain for AI. The question is no longer whether artificial intelligence in insurance works. The data from thousands of live deployments confirms it does. The question is where in the value chain your specific use case sits, and what the implementation pathway looks like.

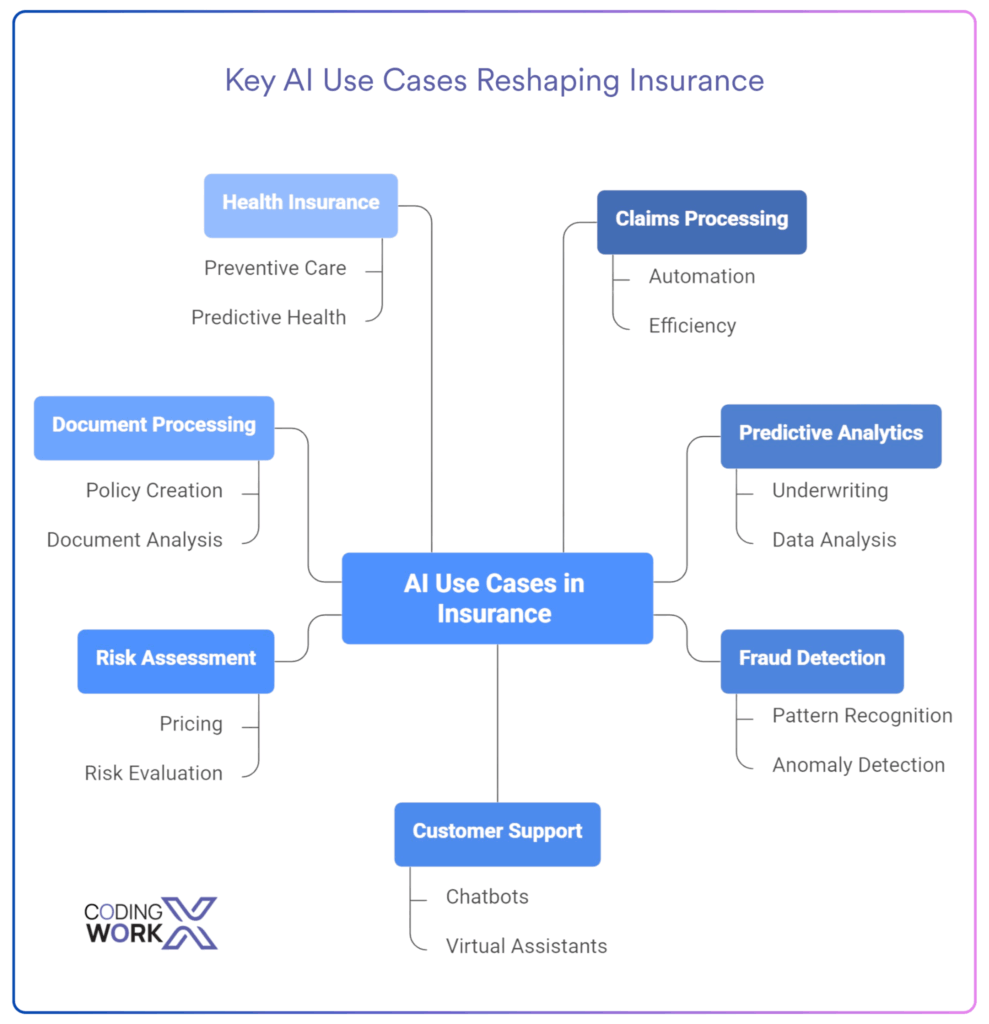

Top AI Use Cases in the Insurance Industry

Here is where AI in insurance industry is delivering real, measurable results, not theoretical potential, but live deployments with documented outcomes.

1. AI-Powered Claims Processing and Automation

Claims processing is where AI in insurance industry has delivered the clearest, most immediate ROI. It is the highest-volume, most document-heavy, most error-prone process in any insurer’s operation, and AI is purpose-built for exactly that profile.

What AI does in claims:

- Reads and classifies unstructured documents like medical records, police reports, photos, repair estimates using natural language processing and computer vision

- Applies trained models to validate coverage, assess damage, and calculate settlement amounts

- Routes routine claims straight through to payment without human review

- Flags complex, high-value, or suspicious claims for adjuster attention

The outcomes:

- End-to-end automation reduces claims processing times by 50–75%, cutting delays from weeks to hours

- AI-driven assessment tools maintain 95% accuracy in claim evaluations

- UK insurer Aviva deployed over 80 AI models, reducing complex case review times by 23 days and saving approximately $82 million annually

For startups building insurtech products, claims automation is the fastest path to a defensible value proposition. For established insurers, it is the use case with the clearest business case and the most mature vendor ecosystem.

Related capability: AI Agent Development enables autonomous claims workflows where AI agents handle end-to-end processing from intake to payment with human escalation only on exceptions.

2. Predictive Analytics in Insurance for Underwriting

Traditional underwriting is slow, expensive, and inconsistently applied. An underwriter reviews an application, applies actuarial tables and judgment, requests additional information, and returns a decision, a process that historically took 3–5 days for straightforward cases and weeks for complex ones.

Predictive analytics in insurance has fundamentally changed this. Machine learning models trained on historical claims data, demographic signals, behavioral patterns, IoT device data, and third-party enrichment sources can now produce risk scores in real time with documented accuracy that exceeds manual review on standardized cases.

What predictive analytics in insurance delivers for underwriting:

- Real-time risk scoring at application submission, not after a multi-day review cycle

- Improved mortality estimation accuracy by 30% in life insurance applications

- McKinsey reports AI-driven underwriting boosts conversion rates by 10–20%, improving profitability while maintaining or improving loss ratios.

The shift this creates: Underwriters move from data gatherers to exception handlers. The model processes standardized applications. Human expertise focuses on the non-standard, high-value cases where judgment genuinely matters.

For insurers evaluating predictive analytics in insurance for underwriting, the critical success factor is data quality. Models trained on biased or incomplete historical data will encode those biases into automated decisions, a regulatory and reputational risk that requires careful governance from the start.

3. AI-Powered Fraud Detection

Traditional fraud detection relies on rules-based systems, flagging claims that match known fraud patterns. The problem: sophisticated fraud evolves faster than rule libraries, and rules-based systems generate high false-positive rates that slow legitimate claims.

AI for insurance companies has shifted fraud detection from reactive to predictive. Machine learning models identify anomalous patterns across thousands of variables simultaneously. claim timing, claimant behavior, provider billing patterns, geographic clusters, and network relationships in ways that no rules-based system can replicate.

Generative AI’s emerging role: 72% of cyber insurers now use generative AI to simulate attack scenarios and stress-test their underwriting models against novel fraud patterns, a capability that did not exist at scale two years ago.

For AI for insurance companies building fraud detection capabilities, the most effective architectures combine supervised models (trained on confirmed fraud cases) with unsupervised anomaly detection (which catches patterns that do not match known fraud types).

4. Conversational AI in Insurance for Customer Support

It is also one of the most consistent sources of customer dissatisfaction — long wait times, inconsistent answers, and handoffs between agents who have to re-explain the same situation from the beginning.

Conversational AI in insurance industry, built on large language models with insurance domain training and integrated with policy management systems, changes this equation fundamentally.

What conversational AI in insurance delivers:

- 24/7 policy inquiry resolution without agent involvement

- Instant claim status updates, payment processing, coverage explanations, and policy modification guidance

- Natural language processing that understands context across a conversation, not just keyword matching

- AI customer support in insurance consistently reduces customer service costs by 20–40% while improving resolution times

- Application of AI in customer service improves customer satisfaction rates by 15–20% through faster and more accurate query resolution

The nuance that matters for startups and SMBs: Conversational AI in insurance is most effective when it is designed around specific, high-volume customer intents like claim status, policy renewal, coverage questions, and billing inquiries rather than built as a general-purpose chatbot. The narrower the scope, the higher the resolution rate, and the better the customer experience.

CodingWorkx’s AI Chatbot Development Services build domain-specific conversational AI systems trained on your policy data, claim workflows, and customer interaction history, not generic chatbot templates.

5. AI-Powered Insurance Solutions for Risk Assessment and Pricing

Usage-based insurance (UBI) and dynamic pricing have been promised for years. What made them difficult to execute was the data pipeline, collecting granular behavioral data, processing it in real time, and translating it into pricing decisions at the individual policy level. AI-powered insurance solutions have made this operationally tractable.

Live examples:

- Telematics-based auto insurance: driving behavior data (acceleration, braking, speed, time of day) feeds ML models that price individual risk in real time

- Smart home sensor data informing homeowners’ insurance pricing — water leak sensors, smoke detectors, security systems

- Wearable health device data shaping life and health insurance products, where regulators permit it

The business outcome: AI-powered insurance solutions for pricing allow insurers to attract lower-risk customers with personalized premiums, improve loss ratios, and build product differentiation that generic pricing models cannot match.

6. Generative AI in Insurance for Document Processing and Policy Creation

Generative AI in insurance is moving past the hype stage and into production workflows — particularly in document-heavy processes where the volume of content exceeds human capacity to review.

Live use cases for generative AI in insurance:

- Automated policy document generation — producing personalized policy language from structured data inputs, reducing manual drafting from hours to minutes

- Loss run processing — automatically summarizing and structuring historical claims data from unstructured documents for underwriter review

- First Notice of Loss (FNOL) document extraction — pulling structured data from photos, written descriptions, and voice transcriptions submitted at claim initiation

- Regulatory filing generation — drafting compliance documents from structured data with human review before submission

- AI copilots in enterprises for internal knowledge management — underwriters and adjusters asking natural language questions across the organization’s entire policy and claims knowledge base

NLP technologies are automating claims document processing, with leading firms reporting reductions in manual effort by 80%. For insurers with high document volume, generative AI in insurance is the fastest path to measurable operational efficiency.

Our Generative AI Development Services help insurers build production-grade GenAI workflows, from document extraction and summarization to customer-facing personalization engines.

7. AI Trends in Insurance Industry: Preventive and Predictive Health Insurance

This is the use case that moves insurance from reactive to proactive, and it represents the most significant long-term transformation of the AI trends in insurance industry landscape.

Traditional health insurance pays after illness. Predictive care AI uses behavioral and biometric data to identify risk before claims materialize, enabling interventions that prevent the claim entirely.

What this looks like in practice:

- Continuous risk monitoring through wearable device data

- Predictive models identifying high-risk patients for proactive outreach

- AI-driven wellness programs tied to premium adjustments

- Predictive care AI identifies patients likely to need specific treatments 12–18 months before symptoms present

For health insurers and digital health startups, predictive analytics in insurance applied to care management is the highest-impact strategic investment available both for loss ratio improvement and for building a differentiated customer proposition.

Key Benefits of AI for Insurance Companies

Across all the use cases above, AI for insurance companies delivers measurable impact across four dimensions:

1. Operational Efficiency

Claims cycle times cut by 75%. Underwriting decisions in 12.4 minutes versus 3–5 days. Document processing was reduced by 80% in manual effort. These are not projections; they are documented outcomes from live deployments.

2. Financial Performance

AI-enabled insurers in Capgemini’s intelligence trailblazer category achieve 21% higher revenue growth. Fraud prevention alone is projected to save P&C insurers $80–$160 billion by 2032. Claims handling cost reductions of 30% are projected across the industry by Gartner.

3. Customer Experience

AI-powered customer experience in insurance consistently delivers 15–20% improvements in satisfaction scores through faster resolution, 24/7 availability, and personalized communication.

4. Risk Management

Predictive analytics in insurance improves underwriting accuracy, reduces loss ratios, and enables proactive fraud prevention. The shift from reactive claims payment to predictive risk management is the fundamental strategic transformation that AI enables.

AI in Insurance Industry: Implementation Challenges to Anticipate

Honest guidance requires acknowledging the challenges as clearly as the benefits.

1. Data Quality and Access:

AI models are only as good as the data they are trained on. Legacy insurers often have decades of valuable claims and underwriting data locked in systems that are difficult to extract, inconsistently structured, and incomplete. Data remediation is frequently the most time-intensive part of any AI implementation and the part most often underestimated in project scopes.

2. Regulatory and Explainability Requirements:

Insurance is a regulated industry, and AI-driven decisions in underwriting and claims are subject to fairness, explainability, and audit requirements that vary by jurisdiction.

3. Legacy System Integration:

Most established insurers run on legacy core systems that were not built for real-time data exchange with modern AI infrastructure. Integration complexity is consistently the largest single source of implementation delays and cost overruns.

4. Talent and Change Management:

Adjusters, underwriters, and customer service agents whose workflows are changing need structured training, clear communication, and role redefinition, not just new software.

5. The Measurement Gap:

42% of insurers track no AI metrics at all. Organizations that cannot measure the impact of their AI implementations cannot improve them and cannot build the internal case for scaling. Establishing clear KPIs before deployment is a prerequisite, not an afterthought.

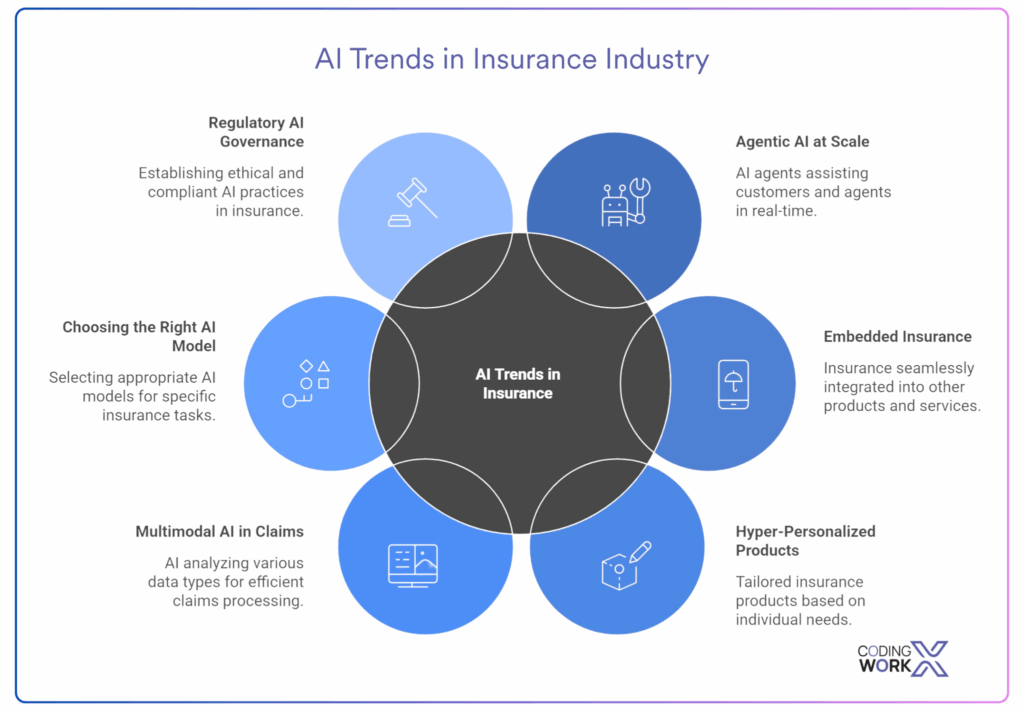

AI Trends in Insurance Industry: What Is Coming Next

The AI trends in insurance industry in 2026 and beyond are not speculative; they are extensions of what the leading insurers are already building.

1. Agentic AI at Scale

2026 marks the shift from AI tools (which assist humans) to AI agents (which complete tasks autonomously). In insurance, this means AI agents that handle FNOL to payment end-to-end for routine claims, agents that manage policy renewal communications without human involvement, and AI copilots in enterprises that give underwriters and adjusters real-time decision support across the full knowledge base of the organization.

AI agent development for insurance requires careful workflow design — defining exactly where autonomous action is appropriate and where human judgment must remain in the loop.

2. Embedded Insurance Powered by AI

AI makes it economically viable to offer insurance at the point of purchase — when someone books a flight, rents a car, or buys a high-value item. AI-powered insurance solutions assess risk and generate a personalized quote in milliseconds, at the moment of maximum purchase intent. This embedded insurance model is expanding rapidly across eCommerce, travel, and fintech.

3. Hyper-Personalized Products

The trajectory of predictive analytics in insurance points toward individual-level risk pricing for a much broader set of insurance products. Rather than pooled risk categories, AI enables granular personalization — different pricing, different coverage terms, and different product structures for each customer based on their specific behavioral and risk profile.

4. Multimodal AI in Claims

Computer vision, voice AI, and large language models are increasingly combined in claims workflows. A customer submitting a claim can photograph damage, record a voice description, and submit documents, and AI processes all three simultaneously, extracting structured data from each modality, cross-validating them, and producing a claim assessment that previously required a field adjuster visit.

5. Choosing the Right AI Model for Insurance Workflows

As the choice of foundation models expands—GPT-4o, Claude, Gemini, Llama, domain-specific fine-tuned models, insurance organizations face increasingly complex decisions about which model to deploy for which workflow. Choosing the right AI model for insurance is not a one-size-fits-all decision. Claims document extraction, customer-facing conversational AI, fraud pattern detection, and underwriting risk scoring each have different accuracy, latency, cost, and explainability requirements that point to different model architectures.

Good to read: Top AI Models Businesses Should Explore

6. Regulatory AI Governance as a Competitive Advantage

The insurers that built governance frameworks, audit trails, and model risk management in 2025 will be the ones who can scale AI fastest in 2026 and beyond, because they will not be stopped by regulatory action. Compliance-by-design is shifting from a burden to a strategic differentiator.

How to Get Started with AI in Insurance: A Practical Framework for Startups, SMBs, and Enterprises

The biggest mistake in adopting AI in insurance industry is starting with technology instead of starting with a business problem.

Step 1: Identify the highest-value problem in your specific operation.

Claims volume too high for the current team? Fraud losses eroding margins? Customer churn driven by service experience? Each problem maps to a different AI application with a different build or buy decision.

Step 2: Audit your data.

AI models require training data. Before scoping an implementation, assess what data you have, its quality, its completeness, and what it would take to make it AI-ready. This step consistently surfaces the work that enables everything else.

Step 3: Start with a bounded use case.

The insurers making the fastest progress are those that define a specific, measurable workflow, routine auto claims processing, for example; prove AI performance against clear KPIs, and then expand. Broad, enterprise-wide AI transformations that try to do everything simultaneously consistently underdeliver.

Step 4: Define your build vs. buy vs. partner decision.

Some AI capabilities are available via SaaS platforms with insurance-specific training. Others require custom development against your proprietary data and workflows. The decision depends on how differentiated the capability needs to be and whether off-the-shelf solutions can meet your accuracy and integration requirements.

Step 5: Build measurement infrastructure before deployment.

Set KPIs. Instrument the workflow. Establish baseline performance before the AI goes live so you can measure actual improvement versus projection.

Whether you are an insurtech startup building AI-powered insurance solutions from the ground up or an established insurer embedding AI development services into existing workflows, the framework is the same: problem first, data second, technology third.

Why Choose CodingWorkx for AI in the Insurance Industry

CodingWorkx is an AI agent development company that builds production-grade AI systems for regulated industries, including insurance, fintech, and healthcare. Our work spans conversational AI solutions for customer-facing insurance applications, generative AI applications for document processing and claims automation, and end-to-end custom AI development for insurers who need AI built around their specific data, workflows, and compliance requirements.

We do not start with a generic AI platform and map it to your use case. We start with your business problem, design the architecture that fits your data maturity and integration environment, and build toward measurable KPIs. Our custom LLM development capability means we can fine-tune foundation models on your proprietary policy and claims data — not just connect to a public API.

If you are evaluating AI for your insurance business, the right starting point is a technical discovery session, not a product demo.

Frequently Asked Questions

1. What is AI in the insurance industry, and why does it matter right now?

AI in insurance industry refers to the deployment of machine learning, natural language processing, computer vision, predictive analytics, and generative AI across core insurance workflows, underwriting, claims, fraud detection, customer service, and product design.

2. What are the most impactful AI use cases in the insurance industry for a startup or SMB?

For an insurtech startup or SMB insurer, the highest-ROI AI use cases in the insurance industry are conversational AI in insurance for customer support, AI-powered claims automation, and fraud detection.

3. How does generative AI in insurance differ from traditional AI applications?

Traditional AI in insurance industry is largely predictive and classificatory; it takes structured inputs and produces a risk score, a fraud flag, or a routing decision. Generative AI in insurance produces new content: policy documents, claim summaries, customer communications, loss run analyses, and regulatory filings. It processes unstructured inputs (photos, voice recordings, free-text descriptions) and generates structured outputs. The operational implication is that generative AI in insurance is most transformative in document-heavy workflows where the volume of content exceeds human processing capacity—FNOL extraction, policy generation, compliance documentation, and internal knowledge management via AI copilots in enterprises.

4. What is conversational AI in insurance, and how is it different from a basic chatbot?

Conversational AI in insurance is a domain-specific natural language interface built on large language models, integrated with your policy management, claims, and CRM systems, and trained to understand insurance-specific intents. Conversational AI understands context across a conversation, handles variation in how customers phrase the same question, and accesses live policy and claim data to provide personalized, accurate responses.

5. How long does it take to implement AI for insurance companies?

The timeline depends heavily on scope and data readiness. A conversational AI for customer support, if your policy and claim data are reasonably structured, can be live in 8–14 weeks.

6. What are the AI trends in insurance industry that will define the next three years?

The AI trends in insurance industry that will have the most operational impact between 2026 and 2029 are agentic AI handling end-to-end claims and policy workflows without human involvement for routine cases; multimodal AI combining computer vision, voice, and language models for claims assessment; hyper-personalized underwriting driven by behavioral and IoT data; embedded insurance at the point of purchase enabled by real-time AI risk scoring; and the emergence of explainable AI governance as a regulatory requirement rather than a best practice.